Today, Tuesday, May 5, 2026, the Reserve Bank of Australia (RBA) sent a clear message to every property investor in the country: the "easy mode" of the last decade is officially dead.

By hiking the cash rate to 4.35%: the third increase we’ve seen already this year: the RBA has effectively told property owners that the fight against 4.6% headline inflation is far from over. With an 8-1 split vote and fuel price shocks continuing to rattle the economy, the central bank isn't pulling any punches.

If you are currently holding a standard investment property with a single tenant, your portfolio just failed its stress test.

It’s time to stop pretending that "long-term capital growth" will pay your mortgage today. In 2026, cash flow isn't just a bonus; it’s your only survival strategy.

The Brutal Math of 4.35%

Let’s look at the reality of this hike. This isn't just a headline on the news; it’s a direct hit to your monthly cash flow.

For the average Melbourne investor with a $750,000 mortgage, this latest move adds roughly another $240 to your monthly repayments. When you stack that on top of the two previous hikes in 2026, you’re looking at a massive hole in your budget that didn't exist in January.

Here is the "Legacy Investor Trap" that most people are falling into:

They think they can simply pass these costs on to their tenants.

Data shows that for every $850 increase in monthly mortgage costs, the average Australian landlord is only able to extract about $25 to $30 extra in rent. The math simply doesn't work. If your mortgage goes up by $250 and your rent goes up by $30, you are bleeding $220 every single month.

Relying on a single family to cover a 2026 mortgage is no longer a viable strategy. It’s "Accidental Investing," and it’s the fastest way to a forced sale.

The Death of Single-Tenancy

For years, the "mums and dads" investment model was simple: buy a 3-bedroom house in the suburbs, find a nice family, and wait 10 years.

That model is now a liability.

When you have one tenant, you have one point of failure. If that tenant loses their job, moves out, or: more likely: simply cannot keep up with the skyrocketing cost of living, your income drops to zero. Meanwhile, your 4.35% mortgage interest keeps compounding.

This is what we call the "Stress Test Failure." Your property cannot withstand the pressure of rising rates because its income potential is capped by the earning power of a single household.

At AZ Property Solutions, we call this the "Single-Tenancy Ceiling." To break through it, you need to change the way you look at a piece of dirt.

The Solution: Income Insurance Through Density

If you want to survive the RBA's hawkish streak, you need to stop thinking about "houses" and start thinking about "yield-generating assets."

The smart money in 2026 is moving toward high-yield density. We aren't talking about "fractional" schemes where you own a brick in a building you’ll never see. And we certainly aren't talking about the over-hyped, high-vacancy risks of NDIS or SDA models that are currently flooding the market with empty promises.

We are talking about residential assets designed for the modern rental crisis: Co-living, Rooming Houses, and Dual-Income properties.

1. Co-living: The 5-Rent Check Model

Imagine a standard residential home, but instead of one family paying $600 a week, you have five individual professionals paying $300 each. Suddenly, your $600/week yield jumps to $1,500/week.

This is Co-living. It provides "income insurance." If one tenant moves out, you still have 80% of your income flowing in. You aren't just surviving the rate hike; you’re thriving in it.

2. Rooming Houses: The Yield King

For those looking for a "Cashflow Fortress," Rooming Houses are the ultimate play. These are purpose-built high-yield assets that can generate upwards of 10% gross yield. In a market where the RBA is squeezing every cent, a 10% yield is the difference between a portfolio that grows and one that withers.

3. Dual-Living (Dual Income)

This is the simplest way to double your protection. A Dual-living property allows for two completely separate tenancies on one title: usually a primary residence and a fully self-contained auxiliary unit. Two rents. One mortgage. One set of council rates.

The "Hawkish" RBA vs. Your Portfolio

The 8-1 split vote at today's meeting tells us one thing: the RBA is not your friend. They are focused on headline inflation, not your mortgage repayments.

When inflation is driven by fuel price shocks and global supply chains, the only tool the RBA has is to crush domestic demand by raising your interest rates. They will keep doing this until the "Standard Investor" breaks.

You have two choices:

- Hold and Hope: Keep your single-tenancy property, watch your margins disappear, and hope the RBA cuts rates (spoiler: they probably won't anytime soon).

- Pivot to Yield: Re-strategize your portfolio around assets that are built for high interest rate environments.

Why the "Done-For-You" Model Wins

The biggest mistake investors make when trying to pivot to these high-yield models is trying to do it themselves. Converting a house to a Rooming House or managing a Co-living property requires specialized knowledge of council regulations, fire safety, and tenant management.

At AZ Property Solutions, we provide a complete done-for-you model. We don't just find you a block of land; we build the specific asset class that fits your strategy: whether that's a rooming house in a high-demand Melbourne corridor or a dual-occupancy build that maximizes every square meter.

We handle the complexities so you can focus on the result: a property that pays you more than you pay the bank.

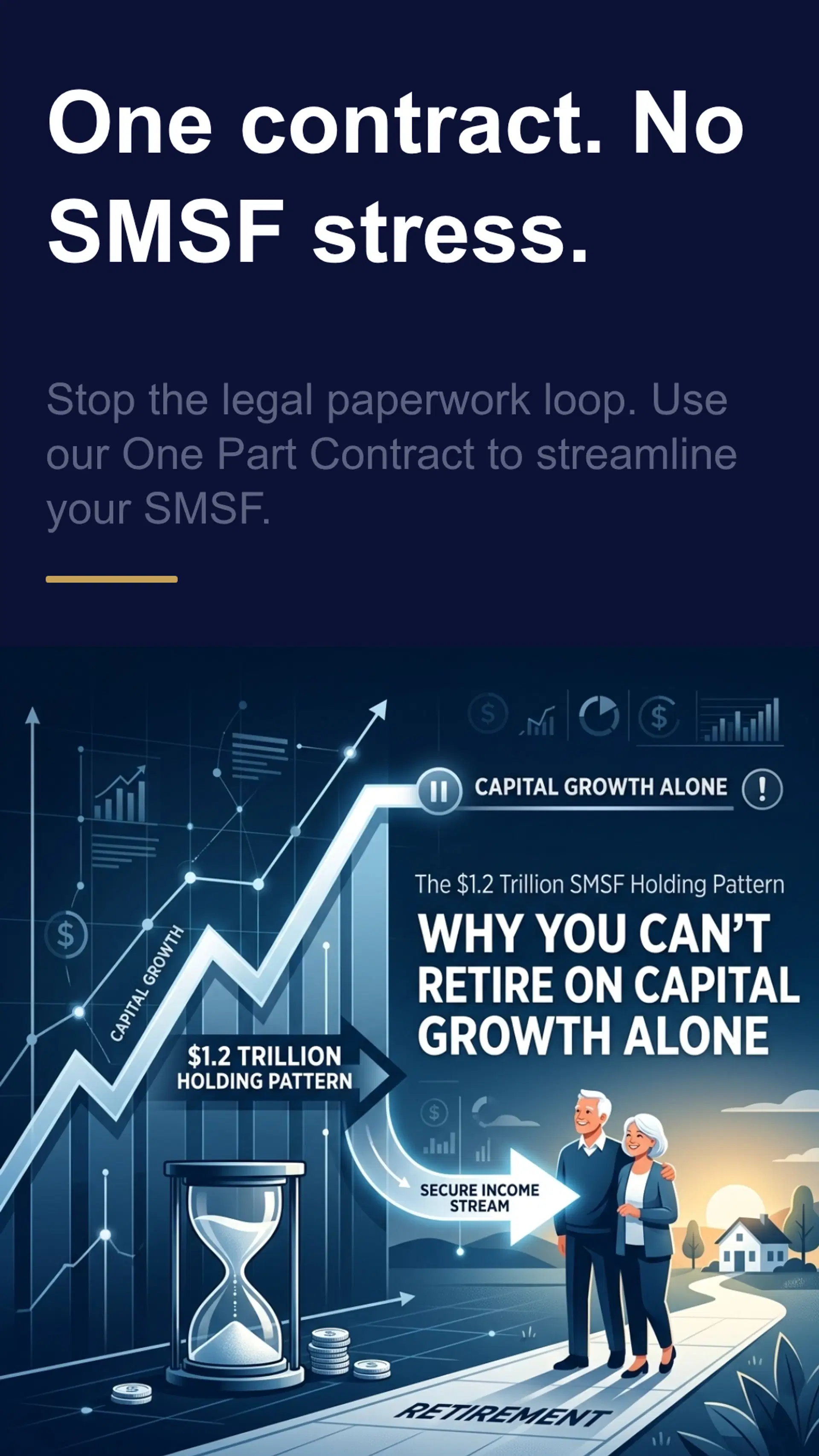

SMSF: The Inflation Lifeline

If you are running an SMSF, today's rate hike is even more critical. You cannot depend on capital growth to fund your retirement when inflation is eating 4.6% of your purchasing power every year.

You need secure, high-frequency income. Our SMSF property investment strategies are designed to strip away the stress. By using a single-contract process for high-yield builds, we ensure your retirement fund isn't just a "savings account with a roof," but a high-performance income engine.

Action Steps for the May 5 Market

Don't wait for the June meeting to see if things "settle down." They won't. Here is what you need to do right now:

- Audit Your Yield: Calculate your "Gap." If your mortgage went up by $250 today, where is that money coming from? If it’s coming out of your pocket, your investment is failing.

- Assess Your Risk: If your one tenant left tomorrow, how many months could you carry the mortgage at 4.35% plus the bank's buffer?

- Explore Density: Look into Co-living and Dual-living options. These are the only residential assets currently outperforming the RBA’s rate hike cycle.

- Ignore the Noise: Avoid the "fractional" and "NDIS" traps. These are often sold as high-yield but come with massive hidden risks and management headaches. Stick to proven residential density.

Ready to Bulletproof Your Portfolio?

The RBA has made their move. Now it’s time for yours.

At AZ Property Solutions, we specialize in helping investors move away from the "One-Check" trap and into high-yield, multi-income assets. Whether you are looking to build a cashflow-positive portfolio from scratch or pivot your existing strategy to survive the 2026 economy, we have the expertise to guide you.

The market has changed. Your strategy must change with it.

Contact the team at AZ Property Solutions today and let’s build you an investment that doesn't just survive the stress test: it passes with flying colors.

Disclaimer: The information provided in this blog post is for general informational purposes only and does not constitute financial or investment advice. Property investment involves risks, and you should consult with professional advisors before making any financial decisions.