Meta Description: The May 2026 Budget just changed the game for property investors. Discover why established homes are becoming a tax trap and why New Build SDA, NDIS, and Co-living are the only way to stay cashflow positive.

URL Slug: is-negative-gearing-dead-established-vs-new-builds-2026

You are losing money on your Victorian terrace.

And you might not even realize it yet.

On May 12, 2026, the Australian government dropped a bombshell that effectively killed the traditional "buy an old house and let the taxpayer fund the loss" strategy.

If you haven’t adjusted your portfolio in the last 12 days, you’re playing a game with outdated rules.

The "Smart Money" isn't panic-selling.

They are pivoting.

They are moving capital into assets that don’t just survive the new tax regime, they thrive under it.

At AZ Property Solutions, we’ve seen this shift coming.

The era of "Accidental Investing", buying established homes and hoping for capital growth to bail out poor yields, is officially over.

Here is why 2026 is the year of the New Build, and how you can secure your financial future while others are left holding the bag.

The 2026 Negative Gearing Trap

Let’s call it what it is: a direct hit on established residential property.

The new rules are simple but devastating for the unprepared.

From 1 July 2027, negative gearing on residential property will be limited strictly to new builds.

If you buy an established home today (post-May 12), you can only offset those losses against your salary for a limited time.

After July 2027, those losses get locked in a "property bucket."

You can’t use them to lower the tax on your hard-earned wage.

You can only offset them against other property income.

Essentially, the government just made established homes significantly more expensive to hold for the average high-income earner.

The "Grandfathering" Illusion

Many investors think they are safe because they already own property.

Yes, if you owned it before 7:30 PM on May 12, 2026, you are grandfathered.

But what happens when you want to expand?

Or when you want to sell?

The pool of buyers for your established investment property just shrank.

Future investors won't get the same tax breaks you did.

This creates a two-tier market:

- Tax-favoured New Builds that add to the housing supply.

- Tax-penalised Established Homes that only serve as primary residences or low-growth rentals.

The Depreciation Engine: Why New Builds Win

In 2026, depreciation isn't just a "nice to have" tax deduction.

It is the engine room of your cashflow.

Because the government is incentivizing "new supply," new builds retain full negative gearing benefits.

But it gets better.

When you build a new high-yield rooming house or an NDIS-compliant home, your depreciation schedule is massive.

You get to claim the decline in value of the building and the "plant and equipment" (ovens, carpets, blinds) from day one.

In an established home, most of these deductions are already "spent" or unavailable to you as a second or third owner.

The NDIS and SDA Advantage

If you want to beat the "negative gearing cliff," you need more than just tax breaks.

You need yield.

Government-backed Specialist Disability Accommodation (SDA) is the ultimate hedge against the 2026 tax changes.

Why? Because SDA housing is almost always a "new build" that adds to the housing stock.

This means:

- Full Negative Gearing: Offset any losses against your salary indefinitely.

- CGT Choice: When you sell, you can choose between the 50% discount or the new indexation rules: whichever saves you more money.

- Ethical Yield: You aren't just chasing a dollar; you are providing life-changing housing for Australians with disabilities.

We specialize in NDIS/SDA housing because it represents the perfect intersection of government policy and investor ROI.

Co-Living: The Melbourne Yield Play

For those looking at Melbourne real estate, the standard 3-bedroom house in the suburbs is a cashflow nightmare.

High land tax, high interest rates, and now, limited tax deductions.

The smart move? Co-living and Rooming Houses.

By pivoting to a "new build" co-living model in high-demand areas like Murrumbeena or near the Monash University precinct, you aren't just getting one rent check.

You are getting 4, 5, or even 9 individual rent streams.

This transforms a negatively geared "hope" into a positive cashflow powerhouse.

Instead of a 2.5% yield on an old house, we are seeing investors achieve 10% to 12% gross yields on custom-built rooming houses.

Why Location Matters More in 2026

You can't just build anywhere.

The 2026 market is discerning.

We look for "Priority Activity Centres" hand-picked by the government for growth.

Places with infrastructure like the Metro Tunnel or major university expansions.

These locations ensure that even if the tax laws shift again, the underlying tenant demand remains unbreakable.

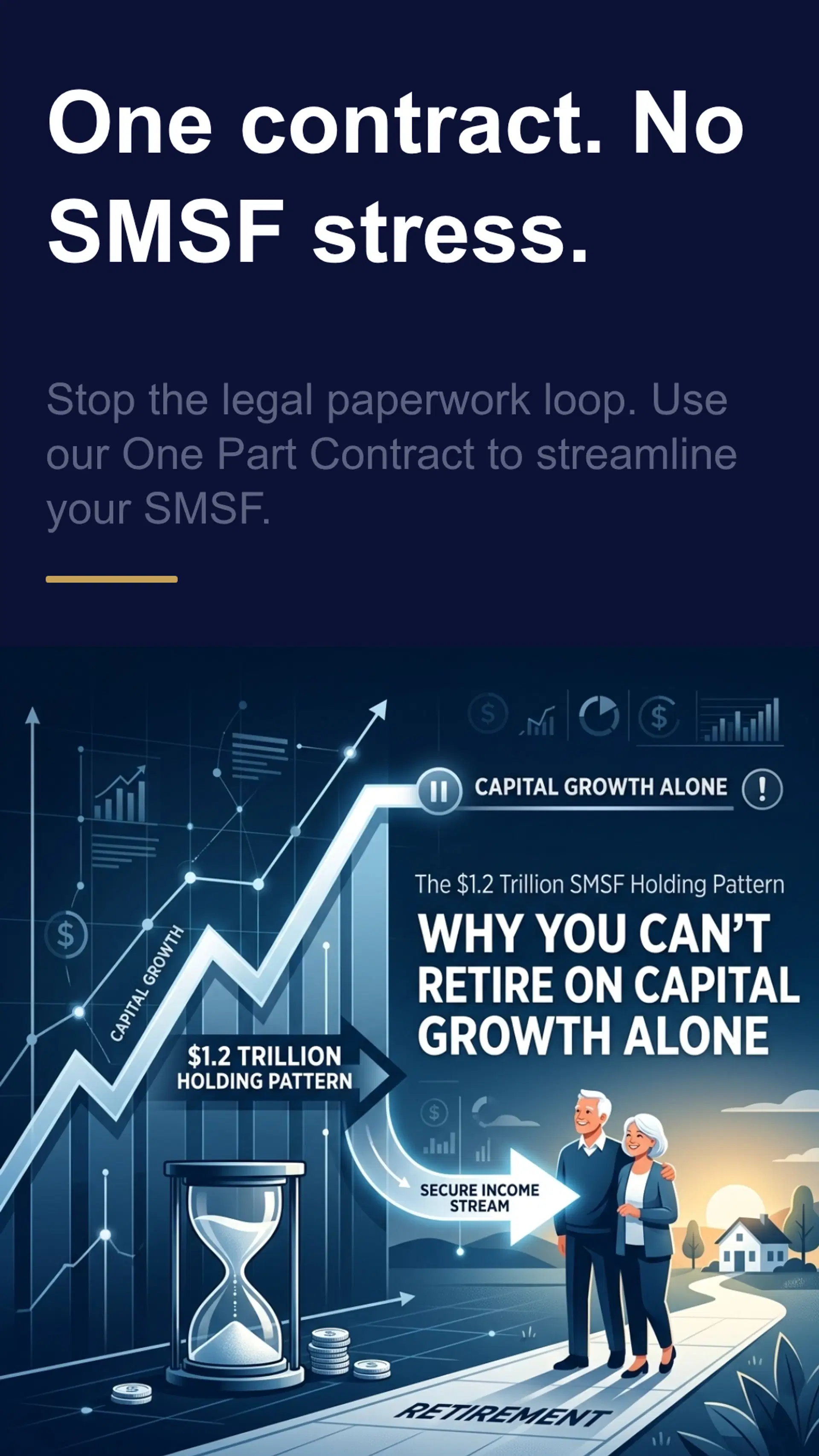

Is Your SMSF Ready?

Many of our clients are using their Self-Managed Super Fund (SMSF) to fund these new builds.

Why? Because retirees cannot depend on capital growth alone.

You need a secure income stream.

With the 2026 budget changes, your SMSF strategy needs to be laser-focused on "New Build" exemptions.

Buying an established unit in your SMSF today is essentially accepting a tax penalty on your future self.

We offer SMSF-friendly property solutions that handle the single-contract requirements and the complex NDIS compliance hurdles for you.

The "Done-For-You" Solution

Most investors are busy.

You have a career, a family, and a life.

You don't have time to interview builders, vet SDA providers, or navigate the new 2026 tax codes.

That’s where we come in.

Our model is simple:

- Selection: We find the high-growth land in Melbourne’s South East or strategic regional hubs.

- Construction: We manage the build of a specialized, high-yield asset.

- Placement: We use our network to find NDIS participants or co-living tenants.

- Management: We ensure your property continues to pay you.

We take the "Accidental" out of investing and replace it with "Property Intelligence."

Frequently Asked Questions (FAQ)

1. Is it too late to buy an established property for negative gearing?

If you haven't signed a contract yet, you are in the transitional phase. You can only negative gear against your salary until June 30, 2027. After that, those losses are locked. For long-term tax efficiency, new builds are now the clear winner.

2. What exactly defines a "New Build" in 2026?

According to the latest budget papers, a new build must "genuinely add to supply." This includes building on vacant land or a knock-down-rebuild where you replace one house with multiple dwellings. A standard renovation does not count.

3. Are NDIS/SDA investments risky with the new laws?

Quite the opposite. The 2026 budget actually protects these investments because they add to the housing supply. The government needs private investors to build these homes, so they have kept the tax perks intact to encourage construction.

4. Can I still invest in international property through AZ Property?

Yes. While the Australian tax focus is on new builds, we still offer diversified portfolios in Dubai and Bali for investors looking for capital growth and tax-efficient structures outside the Australian residential market.

Action Steps for the Smart Investor

- Audit Your Portfolio: Check which properties were bought after May 12, 2026. If they are established homes, run the numbers with your accountant on the "after-tax" cashflow post-July 2027.

- Pivot to Yield: Stop chasing 2% yields. Look into Co-living or SDA models that offer 10%+ returns.

- Use the New Build Exemption: Prioritize any new acquisitions in the "New Build" category to keep your negative gearing and CGT options open.

- Get Expert Guidance: Don't navigate the most significant tax change in a decade alone.

Ready to beat the 2026 tax trap?

Stop gambling with established properties that are bleeding your cashflow.

Join the investors who are already securing high-yield, tax-advantaged new builds.

Book your strategy call with AZ Property Solutions today.

Disclaimer: This information is for educational purposes only and does not constitute financial or tax advice. The 2026 Budget changes are complex; always consult with a qualified accountant or financial planner before making investment decisions.