Your super fund is bleeding potential.

Most Melbourne investors are stuck in the "Residential Rut."

They buy a standard three-bedroom house in the suburbs, cross their fingers for capital growth, and settle for a measly 3% rental yield.

After land tax, maintenance, and management fees, they’re lucky to break even.

Essentially, they are buying an idea: the idea that the market will always go up.

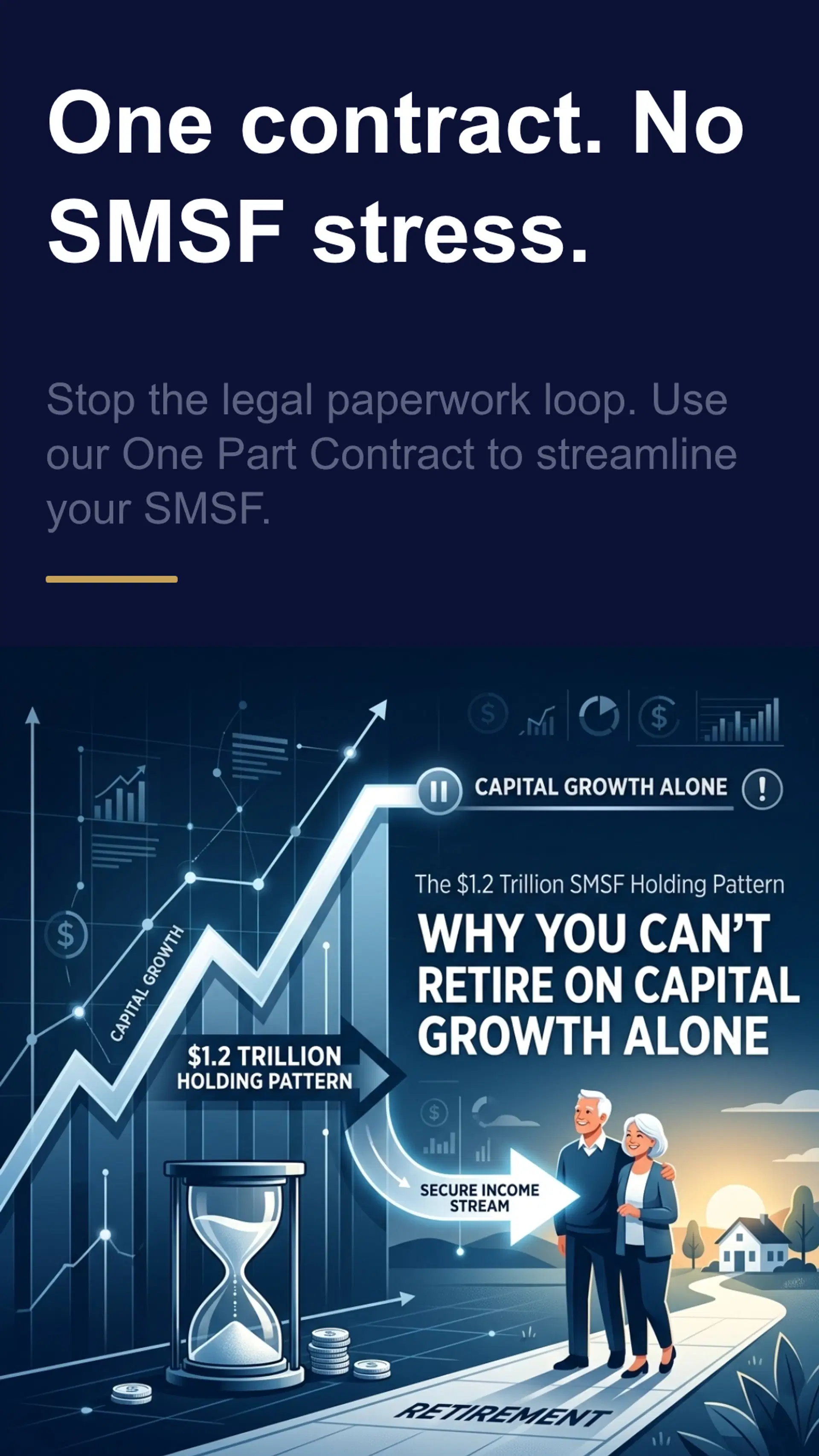

But "Accidental Investing" isn't a retirement strategy. It's a gamble.

If you want to actually retire on your own terms, you need cashflow.

Real, consistent, high-yield cashflow.

And right now, the most powerful vehicle for that inside an SMSF property investment is High-Yield Co-Living.

The Death of the "Single-Tenant" Strategy

The old-school property model is broken for SMSFs.

When you have one tenant, you have one point of failure.

If they leave, your income drops to zero.

If they can't pay the rent, your super fund starts eating itself to cover the mortgage.

Co-living (or high-yield rooming houses) flips the script.

Instead of one family paying $550 a week for a whole house, you have four or five professionals paying $250-$300 each for their own private, high-end suite with shared common areas.

Suddenly, that same property is generating $1,200 to $1,500 a week.

The math isn't just better; it’s transformative.

Why Co-Living is the SMSF Power Move

- Yield Arbitrage: You’re essentially "retailing" the space rather than "wholesaling" the whole house.

- Risk Mitigation: If one tenant leaves, you still have 75-80% of your income flowing in.

- Tax Efficiency: Inside an SMSF, your rental income is taxed at a maximum of 15% (and potentially 0% in the pension phase).

- High Demand: Melbourne’s rental crisis is driving professionals toward high-quality, affordable co-living options.

The $35,000 Entry Point: Fractional Property Investing

The biggest myth in Australian real estate is that you need $200k+ in your super to start buying property.

This "Deposit Trap" keeps thousands of Australians on the sidelines while the market moves without them.

But here’s the truth: You can gain exposure to high-yield co-living assets with as little as $35,000.

Through fractional investment models, your SMSF can buy "units" or "fractions" of a high-performing co-living property.

You get your share of the high rental yields and your share of the capital growth, without the massive debt or the need for a huge deposit.

It’s the perfect way to diversify.

Instead of putting all your eggs in one $800k basket, you can spread your SMSF across multiple high-yield assets.

Why Melbourne is the Yield Battlefield

While Perth and Brisbane have had their moments in the sun, Melbourne remains the strategic choice for savvy co-living investors.

The density of the population and the sheer volume of "key workers" (nurses, teachers, police) who are being priced out of traditional rentals creates a permanent floor for co-living demand.

However, Melbourne's regulations for rooming houses and co-living are strict.

You can't just throw some locks on bedroom doors and call it a day.

That's how you end up in court.

To win in Melbourne, you need "Property Intelligence."

You need purpose-built designs that meet fire safety, council zoning, and tenant expectations.

When done correctly, these properties become "Cashflow Machines" that outperform traditional residential by 2x or 3x.

The AZ "Done-For-You" Model

Let’s be honest: Managing a co-living property is a headache.

Dealing with five individual leases, shared utility bills, and "who left the dishes in the sink" is not a retirement plan. It’s a second job.

At AZ Property Solutions, we specialize in taking that burden off your shoulders.

Our model is end-to-end.

We don’t just find you a property; we build the strategy.

- Selection: We identify high-demand areas where the yield-to-price ratio actually makes sense.

- Compliance: We ensure the build meets all NDIS, SDA, or Rooming House regulations.

- Tenant Placement: We utilize our proven network to find high-quality tenants before the paint is even dry.

- Management: We handle the day-to-day so you can focus on your life, not your leases.

We’ve helped over 50 homeowners with vacant SDA properties secure tenants.

We know what participants want, and we know what investors need.

4 Reasons Why Your SMSF Needs Co-Living Right Now

- Inflation Protection: Rents are indexed. As the cost of living goes up, your SMSF income goes up.

- Debt Reduction: High yields allow you to pay down any SMSF loans (LRBAs) significantly faster than standard residential.

- Social Impact: Especially in the NDIS/SDA space, you aren't just building wealth; you’re providing a home for someone who truly needs it.

- Low Barrier to Entry: With fractional options starting at $35k, there is no excuse to stay in cash or low-yielding stocks.

Action Steps: How to Start

Ready to stop the "Accidental Investing" and start building a real income stream?

Follow this framework:

- Step 1: Check Your Balance. Do you have at least $35,000 in your SMSF? If not, let’s talk about how to get there.

- Step 2: Audit Your Yield. What is your current property portfolio returning? If it’s under 5% net, you are losing money to inflation.

- Step 3: Understand the Compliance. Whether it's co-living or NDIS housing, know the rules of the game in your specific state.

- Step 4: Book a Strategy Call. Don't try to navigate the complex world of SMSF borrowing and co-living regulations alone.

Your Future Self is Watching

Ten years from now, you will either be looking at a healthy, income-producing super fund that pays for your lifestyle, or you’ll be wondering why you stayed in the "Residential Rut" for so long.

The market is moving. The yields are there.

The only thing missing is your decision to act.

Ready to see the numbers for yourself?

Book a strategy call with AZ Property Solutions today and let’s build a high-yield future for your SMSF.

Disclaimer: The information provided in this blog post is for educational purposes only and does not constitute financial, legal, or taxation advice. Investing in property via an SMSF involves risks and complex regulations. We strongly recommend consulting with a licensed financial adviser and SMSF specialist before making any investment decisions.