SEO Meta Description: Stop settling for 3% rental yields. Discover 7 co-living hacks to achieve 8-11% returns in the 2026 Australian property market. Learn how AZ Property Solutions uses purpose-built rooming houses to double your cashflow.

URL Slug: /co-living-investment-hacks-high-yield-australia/

If your investment property is currently returning a 3% gross yield, you aren't an investor.

You are a donor.

In 2026, with inflation and holding costs where they are, a 3% yield means you are effectively paying the bank for the privilege of owning a house.

It’s what we call "Accidental Investing", buying a standard 4-bedroom house in a Melbourne suburb and hoping the capital growth fairy saves your bank account in ten years.

The game has changed.

Smart money is moving away from the "one house, one family" model.

Why bank on a single tenant when you can have five?

Purpose-built co-living (often called Class 1B rooming houses) is the cheat code for investors who actually want their property to pay them.

At AZ Property Solutions, we see the data every day.

Traditional rentals in Melbourne are scraping 3.2% to 4.5%.

Our purpose-built co-living projects are hitting 8% to 11.2% gross yields.

That isn't a small bump; it’s a total lifestyle shift.

Here are 7 co-living cashflow hacks to stop the bleed and start building real wealth.

1. The "Ensuite Upgrade" (Privacy is a Premium)

Most people hear "rooming house" and think of 1970s boarding houses with shared, carpeted bathrooms.

That is a recipe for high vacancy and bad tenants.

The 2026 co-living hack is the Private Suite Model.

Every room must have its own ensuite and, ideally, a small kitchenette.

When you provide a self-contained feel within a shared house, you stop competing with "room rentals" and start competing with "studio apartments."

Renters in Melbourne are desperate for affordable, private spaces.

By adding a $15,000 ensuite to each room during the build, you can often command an extra $100 per week, per room.

In a 5-room house, that’s $26,000 extra per year.

The math is undeniable.

2. Master the Class 1B Compliance

Don’t try to "hack" the law.

Many "accidental investors" try to rent out rooms in a standard house without the right permits.

This is a ticking time bomb of fines and insurance denials.

The real hack is building or converting to Class 1B Building Code standards from day one.

Class 1B involves specific fire safety measures, smoke alarms, and sometimes disability access.

Yes, it costs more upfront.

But it also makes your property a "legitimate" commercial-grade residential asset.

Lenders view compliant rooming houses as specialized income assets.

More importantly, it protects your yield.

A compliant house is a de-risked house.

3. The "Resilient Vacancy" Framework

In a traditional rental, if your tenant leaves, your income hits zero.

You are one bad week away from a mortgage stress headache.

Co-living uses a Multi-Income Stream model.

If you have five tenants and one moves out, you still have 80% of your income coming in.

This hack allows you to be aggressive with your investment strategy because your cashflow never dies.

It’s like having a diversified stock portfolio, but with bricks and mortar.

We focus on high-demand areas like Altona and Ardeer in Victoria, where the "essential worker" population keeps these rooms occupied 98% of the year.

4. Tech-Forward "Smart" Inclusions

If you want the highest-quality professional tenants, you need to provide a "plug-and-play" lifestyle.

The hack here is including high-speed business-grade Wi-Fi, smart locks for every room, and utility-inclusive rent.

Modern tenants hate setting up electricity accounts.

By bundling utilities into the rent and using smart meters to monitor usage, you can charge a premium.

A room that costs $350/week "all-inclusive" is more attractive to a busy professional than a $300/week room where they have to manage four different bills.

It simplifies their life and pads your profit.

5. Strategic Regional Pivot (The Perth/Brisbane Factor)

Don’t get stuck in the Melbourne-only bubble.

While we love Melbourne for long-term stability, the 2026 cashflow hacks often involve looking at Perth or Brisbane.

The entry price in these markets for co-living land is lower, but the rental demand is skyrocketing.

We often guide our investors toward regional hubs where government infrastructure spending is high.

When you combine a lower purchase price with co-living rental rates, your yield doesn't just hit 8%, it can push into the low teens.

Diversifying your portfolio across states is the ultimate shield against local market dips.

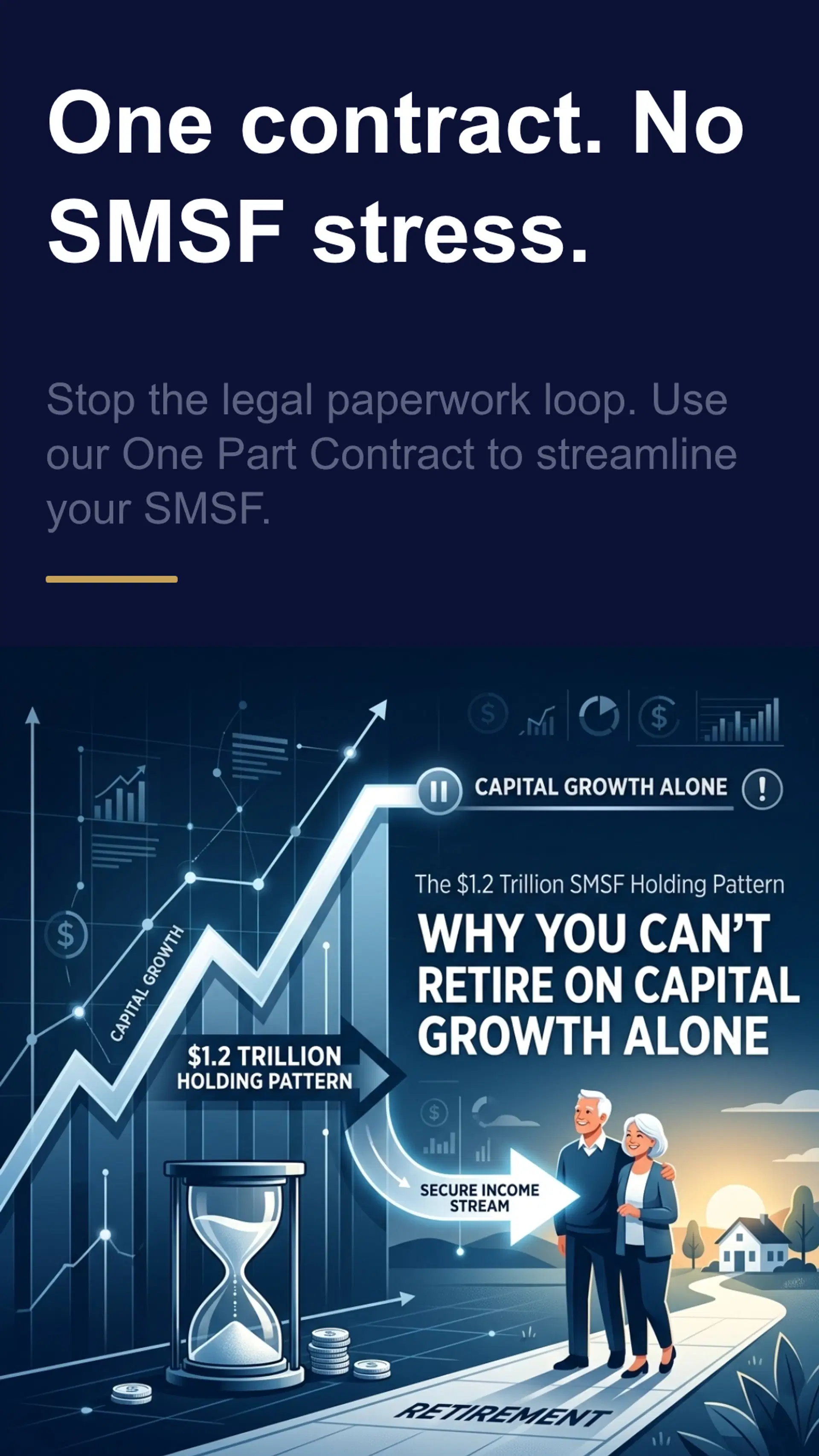

6. SMSF Optimization

Most people have their Super sitting in a "balanced" fund earning peanuts.

The real hack is using a Self-Managed Super Fund (SMSF) to purchase high-yield co-living property.

Because co-living provides such high cashflow, the property often pays off its own debt within the fund much faster than a standard rental.

We specialize in SMSF-friendly property models.

We handle the single-contract requirements that banks need for SMSF lending, making the process seamless.

You aren't just buying a house; you are building a tax-effective retirement machine.

7. The "Done-For-You" Management Hack

The biggest myth about co-living is that it’s a "management nightmare."

It is a nightmare if you try to manage five individual leases yourself while working a full-time job.

The pro hack? Use a specialized co-living manager.

Traditional property managers are great at collecting rent from one family.

They are terrible at managing the "social dynamics" of a co-living house.

You need a manager who understands rooming house law, tenant placement, and common area maintenance.

At AZ Property Solutions, our "done-for-you" model includes the placement network needed to keep your rooms full of the right people.

The Reality Check: Is there a Catch?

We don’t do hype. We do intelligence.

Co-living isn't "set and forget" like a standard house.

There is more wear and tear.

There is more red tape.

There is higher turnover.

But if you are willing to manage those risks through a professional partner, the rewards are double or triple what your neighbor is making.

While they celebrate a 3% capital growth year, you are pocketing a 10% yield plus the growth.

Who is the real winner?

How We Bridge the Gap

At AZ Property Solutions, we don't just sell you a floor plan.

We manage the entire lifecycle.

From selecting the right land in high-yield corridors to navigating Class 1B council approvals, and finally placing high-quality tenants.

We’ve seen the success stories firsthand.

We’ve helped over 50 homeowners with vacant SDA properties secure tenants and worked with dozens of co-living investors to turn underperforming portfolios into cashflow engines.

Whether it’s NDIS/SDA housing with government-backed returns or high-yield rooming houses, we ensure your investment is performing from day one.

Ready to Stop Settling?

The 3% era is over.

The inflation-beating, wealth-building era of co-living is here.

Don't be the investor who looks back in five years and wonders why their portfolio didn't grow.

Let us help you build a property that actually pays you.

[Book Your Strategy Call with AZ Property Solutions Today]

FAQ: Co-living Investment in Australia

Is co-living the same as a boarding house?

Technically, they fall under similar building codes (Class 1B), but the "co-living" model we use is premium. It focuses on high-end finishes, private ensuites, and professional tenants rather than budget accommodation.

Can I use my Super to buy these?

Yes. We offer single-contract builds that are specifically designed to meet SMSF lending criteria. This is one of the most popular ways our clients build their retirement wealth.

What is the minimum investment?

We have entry-level fractional options starting from $35,000, or full "done-for-you" builds starting from approximately $700k depending on the location and model.

What about NDIS/SDA?

SDA (Specialist Disability Accommodation) is a specialized form of high-yield housing. It offers even higher yields (often 10-15%) but requires specific compliance and participant placement. We handle both SDA and standard co-living.

Disclaimer: This information is general in nature and does not constitute financial or legal advice. Property investment involves risks. You should consult with a qualified financial advisor and legal professional before making any investment decisions.