Most property investors in Melbourne are still playing a game from 2004.

They buy an old villa unit, cross their fingers for capital growth, and celebrate a tax refund at the end of the year.

This is what we call "Accidental Investing."

In 2026, it’s not just an outdated strategy: it’s a dangerous one.

With interest rates remaining stubborn and the Federal Government tightening the screws on negative gearing for established properties, the "buy-and-hope" model is dead.

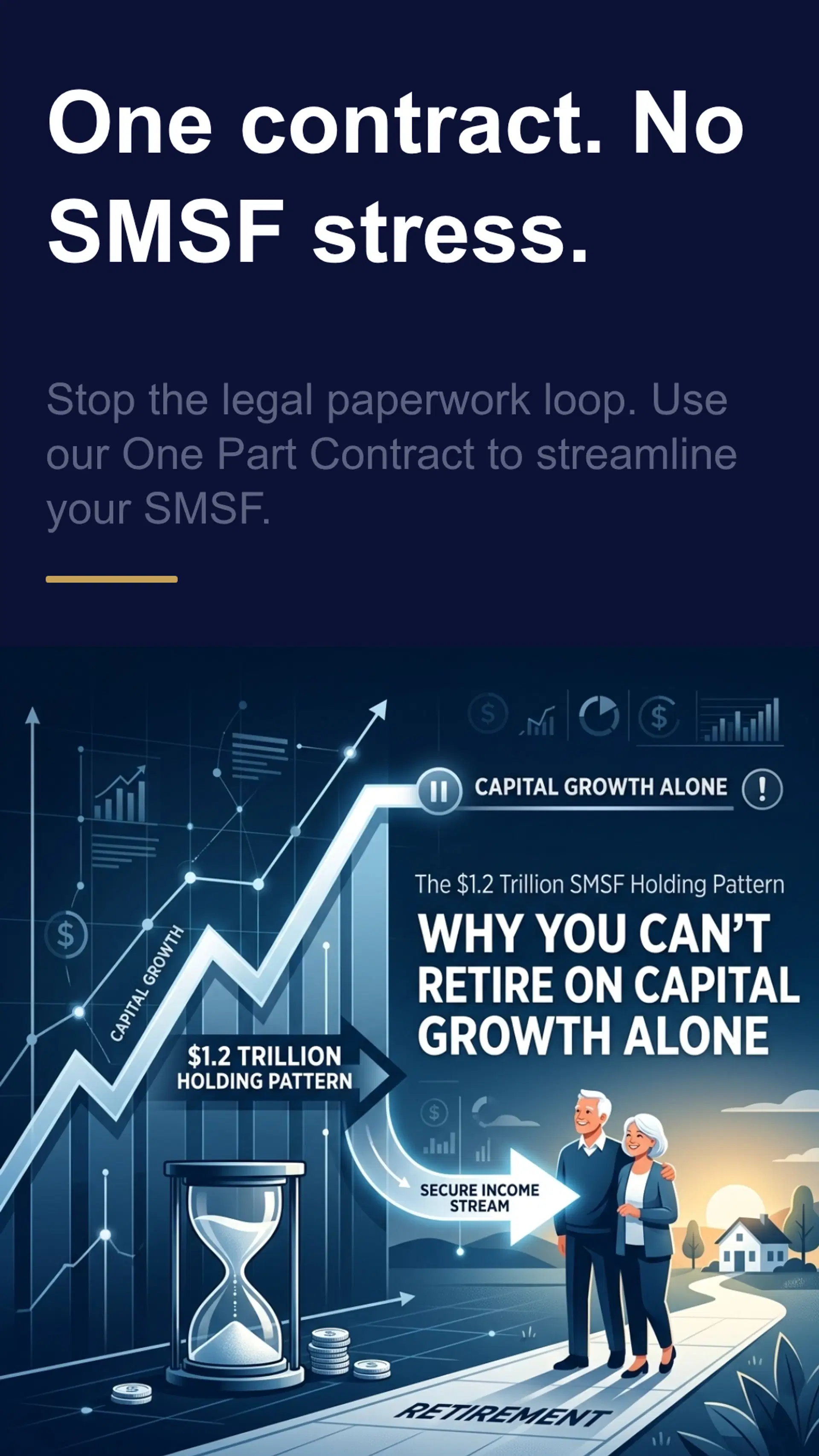

If your strategy relies on losing money every month just to get a fraction of it back from the ATO, you aren't an investor.

You’re a subsidiser for your tenant's lifestyle.

It’s time to talk about why high-yield new builds are the only logical move for your SMSF and your sanity.

The Negative Gearing Trap: A Loser’s Game in 2026

Negative gearing is often sold as a "tax benefit."

Let’s call it what it actually is: A guaranteed monthly loss.

If you are a high-income earner in Melbourne or Sydney, losing $500 a week to save $225 in tax still leaves you $275 out of pocket.

Every. Single. Week.

By 2026, the math has become even uglier.

The new policy shifts (set for full effect in 2027) mean that for future purchases of established residential property, you won’t be able to offset those losses against your salary.

You’ll have to carry them forward to offset future capital gains.

Essentially, you are paying for a "maybe" in ten years' time with "definitely" gone cash today.

Is that a gamble you want to take with your retirement?

Why Your SMSF is Bleeding Out

Investing through a Self-Managed Super Fund (SMSF) changes the rules of the game entirely.

Inside an SMSF, your tax rate is capped at 15%.

When you negatively gear in your own name at a 45% tax bracket, the government "helps" you more.

When you do it inside your SMSF, that 15% tax shield is pathetic.

The SMSF Math is simple:

- You cannot easily fund an SMSF's monthly losses from your own pocket (thanks to contribution caps).

- If the property doesn't pay for itself, it eats your retirement balance alive.

- Retirees cannot eat "capital growth." They need income.

At AZ Property Solutions, we see trustees every week who are one interest rate hike away from their SMSF going into the red.

The solution isn't to stop investing; it's to pivot to assets that actually put money into the fund.

The Loophole: Why New Builds Still Win

The 2026 landscape has a clear winner: New Builds.

While the government is cracking down on the tax benefits of old, "established" houses, new builds are being incentivised to solve the housing crisis.

New builds retain:

- Full Negative Gearing Benefits: If you still want that tax shield, this is the only place left to get it effectively.

- Maximum Depreciation: You can claim the building, the carpets, the ovens: everything. This creates "paper losses" that protect your cash flow without you actually losing money.

- Higher Yields: Modern designs like co-living and NDIS/SDA are built for maximum rental return, not just "market average."

The Yield Kings: NDIS/SDA and Co-Living

If you want to beat inflation and stop worrying about the ATO, you need to look at High-Yield Specialised Housing.

1. NDIS / Specialist Disability Accommodation (SDA)

This isn't just "social impact"; it’s the most robust property play in Australia right now.

The government backs these payments.

The yields are often 10% to 15%+.

We have helped over 50 homeowners secure tenants for vacant SDA properties through our Participant Placement Network.

We don't just build these homes; we ensure they are performing.

It’s a dual-impact model: you get significant positive cashflow, and a person with a disability gets a high-quality, fit-for-purpose home.

2. High-Yield Co-Living and Rooming Houses

Why rent a 4-bedroom house to one family for $600 a week when you can rent 4-5 premium, self-contained suites for $300 each?

The math is undeniable. Co-living is the answer to the 2026 affordability crisis.

It’s how smart investors are hitting 12% ROI while the "Accidental Investors" are struggling with 3% yields in Melbourne’s suburbs.

The Regional Alpha: Perth & Brisbane vs. Melbourne

If you are a Melbourne-based investor, the hardest pill to swallow is that your backyard is currently a yield desert.

The "Alpha" (the outsized returns) is currently in the north and the west.

- Perth: Low entry costs, skyrocketing demand, and yields that make Sydney look like a charity project.

- Brisbane: Infrastructure-led growth and a massive migration shift.

We specialise in identifying these high-yield pockets and delivering a done-for-you model.

From land selection to build completion to tenant placement, we handle the logistics so you don't have to be an expert in Western Australian zoning laws.

Action Steps for the 2026 Investor

Stop chasing tax refunds. Start chasing cash.

Here is your framework for a 2026-proof portfolio:

- Audit Your Yields: If your property is yielding less than 5% gross, it is likely a drag on your wealth in this high-rate environment.

- Look at the SMSF Balance: If you have an SMSF, prioritise "Neutral to Positive" gearing. Your fund should grow via rental income, not just contributions.

- Target "New Build" Incentives: Maximise depreciation and protect yourself from the 2027 negative gearing restrictions on established stock.

- Explore Specialised Models: Research NDIS/SDA housing and Co-living options to bridge the gap between "market rent" and "inflation-beating rent."

Ready to stop bleeding cash?

The "Accidental Investor" wait for things to get better.

The Strategic Investor makes things better by choosing the right assets.

At AZ Property Solutions, we offer an end-to-end expertise managing the entire investment process.

Whether you're looking for low capital entry options starting from $35,000 or high-yield NDIS builds, we have the proven results to back it up.

Let us help you build a portfolio that actually pays you.

Book a Strategy Call with the AZ Team Today

FAQ: Negative Gearing in 2026

Q: Is negative gearing being scrapped?

A: Not entirely. The 2026 policy outlook suggests it will be restricted for future purchases of established residential properties (likely from July 2027), but remains fully accessible for new builds.

Q: Why is SMSF property better for high-yield?

A: Because of the low 15% tax environment, you keep more of the rent. Plus, if you hold the property into the pension phase, your capital gains can potentially be tax-free.

Q: Can I still get high yields in Melbourne?

A: It is significantly harder with traditional residential stock. This is why we focus on rooming houses and NDIS/SDA builds( they create their own yield through specialised demand.)