If you are still waiting for Sydney house prices to double so you can finally retire, you aren't an investor.

You are a gambler.

In May 2026, the game has changed.

The "Buy and Hope" strategy that worked for your parents in the early 2000s is officially dead.

Inflation is sticky, interest rates aren't dropping back to zero, and the cost of living is eating your "paper gains" for breakfast.

Most investors are stuck in what we call The Capital Growth Trap.

They buy a property that loses them $500 a week in holding costs, praying that the market will lift them out of the hole in ten years.

But your bank doesn't care about your "estimated equity" when you're trying to buy groceries or fund your next acquisition.

They care about serviceability.

They care about cashflow.

At AZ Property Solutions, we’ve spent years perfecting the Positive Cashflow Framework.

It’s the only way to build a portfolio that scales without hitting a "serviceability wall" after property number two.

The "Accidental Investor" vs. The Strategic Architect

Most Australians are "Accidental Investors."

They buy a standard 4-bedroom house in a suburb they know, put a standard tenant in it, and hope for the best.

Then they wonder why their portfolio stops growing after one or two purchases.

The reason? Their properties are a liability, not an asset.

An asset puts money in your pocket. A liability takes it out.

If your property is negatively geared, you are effectively subsidising your tenant's lifestyle while the bank holds your hand behind your back.

The Strategic Architect: the investor who wins in 2026: uses a framework designed for high-yield returns from day one.

Phase 1: The Yield Threshold (8% or Bust)

The first rule of our framework is simple: Yield is your shield.

In a high-inflation environment, capital growth is the icing, but cashflow is the cake.

We don't look at properties returning 3% or 4% yields.

Those are "ego plays" for people who like to brag about owning a house in a posh suburb.

To beat inflation and satisfy the banks in 2026, you need to be targeting a minimum gross yield of 8% to 15%.

Where do you find these?

Not in the standard residential market.

You find them in high-performance asset classes like:

- NDIS/SDA Housing: Government-backed yields that can hit 15%.

- Co-Living (Rooming House 2.0): Multiple income streams from a single title.

- Regional Powerhouses: Locations like Perth and Brisbane where the price-to-rent ratio actually makes sense.

Learn more about our high-yield secrets here.

Phase 2: Asset Selection (The Heavy Hitters)

Not all high-yield properties are created equal.

If you buy a high-yield property in a "dying" mining town, you’re just buying a headache.

Our framework focuses on high-yield assets in high-demand growth corridors.

NDIS & Specialist Disability Accommodation (SDA)

This is the gold standard of the Positive Cashflow Framework.

You are providing much-needed housing for Australians with disabilities, backed by Federal Government funding.

The yields aren't just good; they are life-changing.

But it’s not as easy as building a ramp and calling it a day.

The "Accidental Investor" gets burnt here by bad builders or incorrect compliance.

Our done-for-you model handles the compliance, the build, and the tenant sourcing so you just collect the 15% yield.

Co-Living: The Multi-Income Hack

Co-living is the modern evolution of the rooming house.

Instead of one family paying $600 a week, you have three or four professionals paying $350 each.

The math is undeniable.

You are essentially doubling your rental yield on the same piece of land.

Phase 3: Location Arbitrage (Ego vs. Economics)

If you live in Sydney or Melbourne, the hardest part of the framework is leaving your backyard.

Many investors suffer from "Home-Bias."

They want to be able to drive past their investment on a Sunday.

That drive is costing you hundreds of thousands of dollars.

In 2026, the smart money is moving to Perth and Brisbane.

Why? Because the entry price is lower and the rental demand is higher.

We’ve seen Perth outperform the Eastern states consistently because the supply-demand imbalance is so severe.

Chasing capital gains in Sydney is a 2024 strategy.

Chasing cashflow in Perth is the 2026 reality.

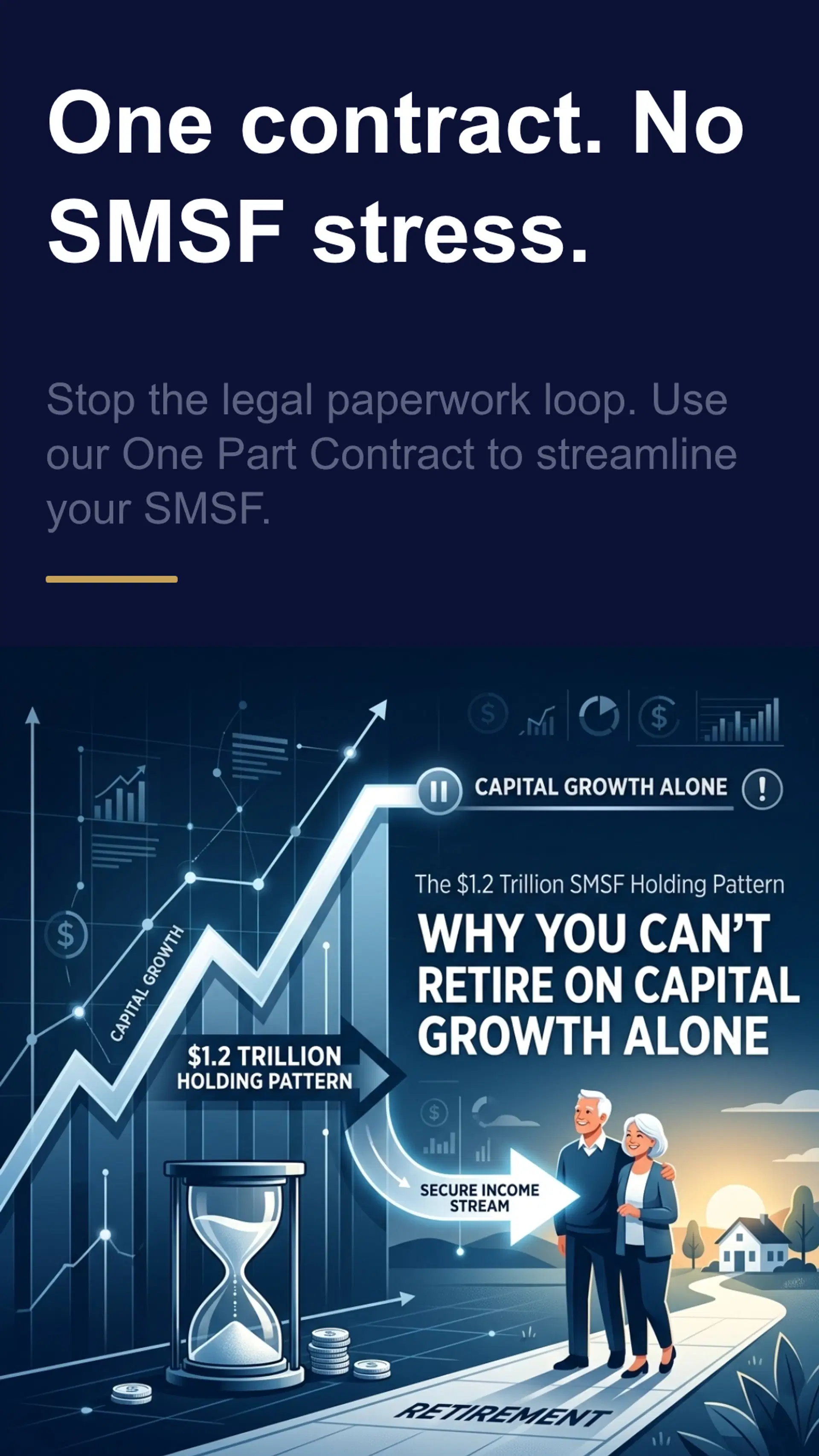

The SMSF Retirement Trap

If you are running an SMSF, the Positive Cashflow Framework isn't just an option: it’s a necessity.

Most SMSFs are sitting on a $1.2 trillion holding pattern of underperforming assets.

You cannot retire on capital growth alone.

You can't sell a brick of your house to pay for a holiday in Europe.

Your SMSF needs income.

By pivoting your super into high-yield property, you create a self-sustaining pension fund that doesn't rely on the volatility of the stock market.

Retirees cannot depend on capital growth alone.

Why Most Investors Fail (And How We Fix It)

Investing in high-yield property is complex.

There are more moving parts than a standard residential buy.

You have to deal with:

- Strict Compliance: Especially with NDIS and Co-living.

- Specialised Lending: Not every bank "gets" high-yield assets.

- Property Management: You need managers who understand per-room or NDIS leases.

Most people try to DIY this and end up with a "lemon" property that sits vacant for months.

That’s where AZ Property Solutions comes in.

We provide a "Done-For-You" model.

We find the land, vet the builders, handle the compliance, and secure the tenants.

You provide the vision; we provide the vehicle.

Action Steps: How to Implement the Framework Today

If you're ready to stop being an "Accidental Investor," follow these steps:

- Audit Your Current Portfolio: If your properties are draining more than $200 a week from your pocket, you have a liability problem.

- Shift Your Metric: Stop looking at "Median House Prices" and start looking at "Gross Rental Yield."

- Explore NDIS/SDA: Understand the government-backed 15% yields. Read the secrets here.

- Go Borderless: Look at Perth and Brisbane for better yield-to-value ratios.

- Get Expert Help: Don't try to navigate NDIS or Co-living regulations alone.

The Bottom Line

The era of easy money is over.

To build wealth in 2026, you need a strategy that generates cash today, not just "potential" wealth tomorrow.

The Positive Cashflow Framework is designed to give you the liquidity to live your life and the serviceability to keep buying more assets.

Don't let inflation erode your hard-earned savings.

Put your money into an asset that works as hard as you do.

Ready to see what a 12% to 15% yield looks like for your bank account?

Let us help you build a portfolio that pays you to own it.

At AZ Property Solutions, we specialise in identifying the high-yield opportunities that traditional agents don't even know exist.

Explore our current high-yield opportunities here.

Disclaimer: Real estate investment involves risks. High yields often come with specific regulatory and management requirements. Always seek professional financial and legal advice before making investment decisions.