Most Australian property investors are playing a losing game.

They buy a standard three-bedroom home in a Melbourne suburb.

They celebrate a 3% rental yield.

Then, inflation hits 4%.

The RBA hikes rates again.

Suddenly, that "investment" is a liability that requires a monthly top-up from their salary.

This is what we call "Accidental Investing."

It’s a strategy built on hope, not math.

If you want to beat the system, you have to stop thinking like a traditional landlord.

The secret isn't finding a "bargain" in a saturated market.

The secret is Specialist Disability Accommodation (SDA) under the NDIS.

We’re talking about yields that can exceed 15%.

We’re talking about government-backed income.

And we’re talking about doing it without the midnight calls about a leaking toilet.

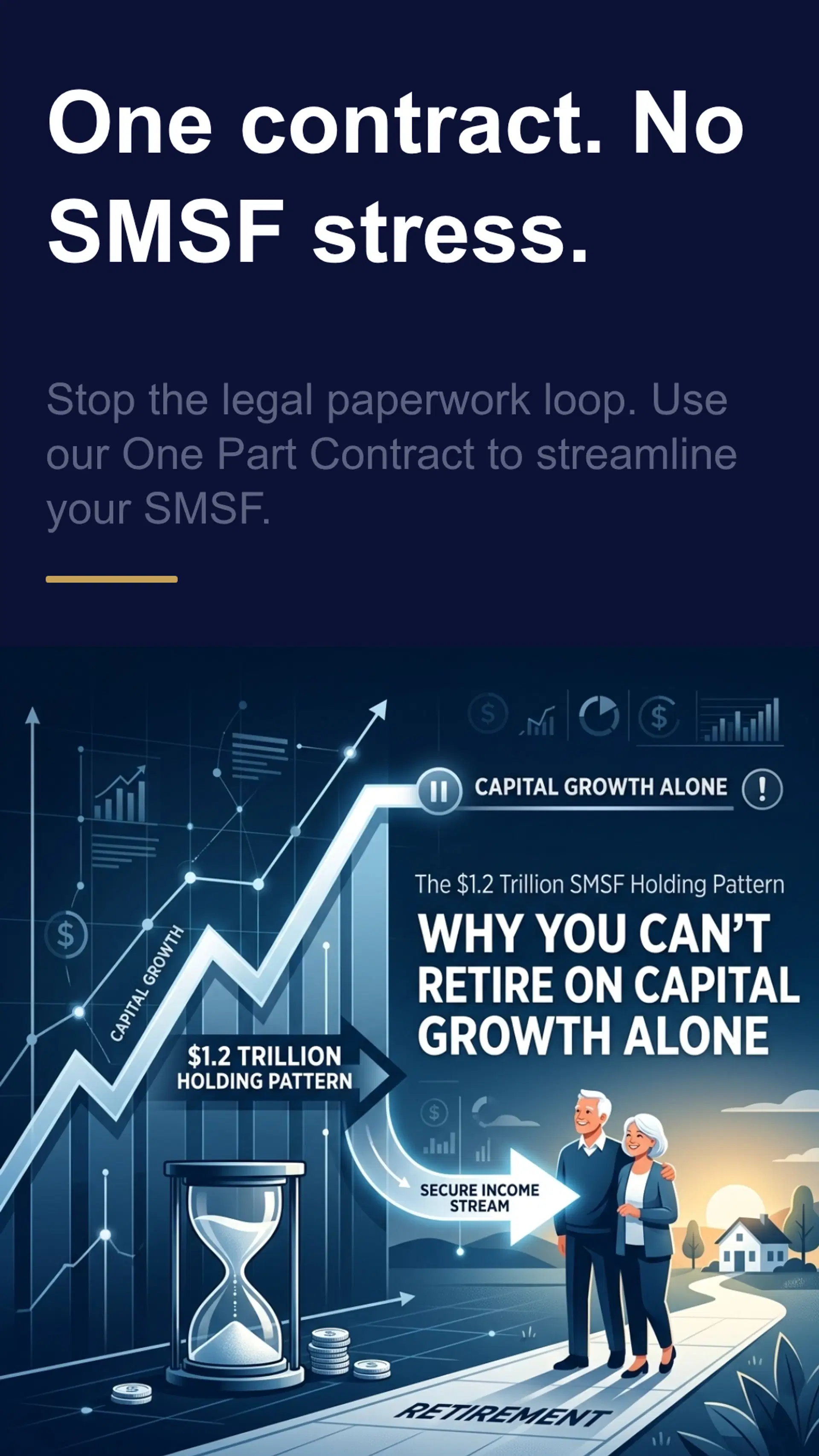

The Yield Trap: Why Your Current Strategy is Broken

Traditional residential property is a capital growth play.

But capital growth doesn't pay the groceries today.

In the current economic climate, cash flow is king.

Most investors are terrified of NDIS property because it sounds "too complex."

They stick to what they know: and what they know is keeping them broke.

They fall into the "Compliance Coma."

They assume that because the yields are high, the risk must be astronomical.

The truth? The risk is only high if you don't know the rules of the game.

At AZ Property Solutions, we don't guess.

We use Property Intelligence to identify the gaps in the market.

Right now, the gap is high-quality, compliant housing for Australians with extreme functional impairment.

The government is literally subsidising the rent to ensure these people have homes.

You aren't just a landlord; you are a solution provider.

The 15% Math: How the Numbers Actually Work

You’ve probably heard people claim NDIS yields are a myth.

They aren't. They are just mathematically different from standard rentals.

In a standard rental, you have one tenant paying market rate.

In an SDA-compliant home, your income is comprised of three parts:

- The Fair Rent Contribution (paid by the participant, capped at 25% of their disability support pension).

- The Commonwealth Rent Assistance.

- The SDA Payment (the big one, paid by the NDIS directly to the provider).

When you build a "High Physical Support" or "Robust" category home, the SDA payment is significant.

In high-demand areas like Perth or parts of Brisbane, a well-designed home with two or three participants can easily generate $100,000 to $150,000 in gross annual income.

On a $700,000 or $800,000 build, that is a 15%+ yield.

Try getting that from a townhouse in Glen Waverley.

Why You Hate Being a Landlord (And How to Fix It)

Most investors suffer from "Landlord Fatigue."

They hate the vacancy rates.

They hate the property managers who don't care.

They hate the "tenant from hell" who ruins the carpets.

SDA property flips this script.

When you work with a professional SDA Provider, they handle the participant management.

The participants are looking for "forever homes."

Vacancy rates in the SDA sector are driven by poor design, not a lack of demand.

If you build the right product in the right location, your "tenant" stays for years, not months.

The Perth/Brisbane vs. Melbourne Divide

We see a lot of Melbourne investors making the "Local Bias" mistake.

They only buy what they can drive past on a Sunday.

This is a path to mediocrity.

Melbourne is great for long-term capital stability, but the entry price for SDA is high.

If you want the 15% yield, you need to look where the land-to-build ratio makes sense.

Perth is currently a goldmine for NDIS investments.

The land is cheaper, the demand for "Robust" housing is surging, and the construction timelines are finally stabilising.

Brisbane offers a similar "sweet spot" for investors looking for regional growth.

The "Done-For-You" Model: Your Shield Against Mistakes

You shouldn't be trying to manage an NDIS build yourself.

This is where the "DIY Disaster" happens.

There are over 500 pages of compliance standards for SDA housing.

If your door frames are 10mm too narrow, the property cannot be registered.

If your light switches are at the wrong height, you lose your 15% yield.

You end up with a very expensive, very weirdly designed standard house that no one wants.

AZ Property Solutions offers a one-part contract model.

We handle the land acquisition.

We handle the SDA-certified builders.

We connect you with the registered NDIS providers.

We basically hand you the keys to a cash-flow machine.

Our expertise is your insurance policy against government red tape.

SMSF: The Ultimate Tax Shield for High Yields

If you have a Self-Managed Super Fund, NDIS property is a cheat code.

Retirees cannot live on capital growth. You can’t eat "potential equity."

You need cash flow to fund your lifestyle.

By using your SMSF to fund an NDIS build, you are funnelling that 15% yield into a low-tax environment.

It’s the most efficient way to accelerate your retirement timeline.

We specialise in SMSF property investments that take the stress out of the compliance audit.

3 Myths That Keep Investors Poor

Myth 1: "The NDIS is being cut, so the yields will disappear."

The NDIS is a non-partisan, essential service.

While the government is looking to trim "fat" in administrative costs, they are actually increasing the focus on permanent, high-quality housing.

Why? Because it is cheaper for the government to house someone in a purpose-built SDA home than in a hospital bed or an aged care facility.

Your investment actually saves the taxpayer money.

Myth 2: "It’s too hard to find tenants."

It’s only hard if you build a "Zombie Property."

A Zombie Property is an SDA home built in the middle of nowhere with no access to transport or medical services.

If you use data-backed site selection: like our Pomegranate Drive projects: the demand is already there before the slab is even poured.

Myth 3: "I can’t afford it."

Many investors don't realize they can leverage co-living or rooming house strategies if a full SDA build is out of reach.

Or, they use the equity in their current home to fund the deposit for a High-Yield SDA Home.

Action Plan: Your 5-Step Move to 15% Yields

Don't be a spectator. Follow this framework to get started:

- The Reality Check: Audit your current portfolio. If your net yield is under 4%, you are losing money to inflation.

- The Capacity Test: Talk to a broker who understands NDIS lending. Standard banks often struggle with this; you need a specialist.

- The Strategy Session: Decide on your location. Are you chasing the growth in Perth or the stability of Brisbane?

- The Partnership: Don't hire a standard builder. Partner with a "Done-for-you" specialist like AZ Property Solutions.

- The Execution: Secure a one-part contract to streamline your SMSF or personal investment.

The Bottom Line

The window for high-yield NDIS investments won't stay open forever.

As more institutional money flows into the sector, yields will eventually compress.

The "early movers" who act now are the ones who will secure their financial freedom while others are still arguing about interest rates.

Stop being an "Accidental Investor."

Start building a portfolio that actually pays you.

Whether it's triple-key living or a rare SDA cashflow home, the opportunity is staring you in the face.

{kind=link}

Ready to Secure Your 15%?

We don't just talk about yields; we deliver them.

At AZ Property Solutions, we take the "headache" out of the landlord experience.

From site selection to participant move-in, we are your partners in property intelligence.

Contact AZ Property Solutions Today to see our current high-yield opportunities and learn how we can help you beat the inflation trap.

Let’s stop dreaming about retirement and start funding it.

Disclaimer: All investment involves risk. Yields are based on current NDIS legislation and participant funding levels. We recommend seeking independent financial and legal advice before making any property investment.